The past six months have been a windfall for Coupang’s shareholders. The company’s stock price has jumped 40.7%, setting a new 52-week high of $31.23 per share. This performance may have investors wondering how to approach the situation.

Following the strength, is CPNG a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Does Coupang Spark Debate?

Founded in 2010 by Harvard Business School student Bom Kim, Coupang (NYSE:CPNG) is an e-commerce giant often referred to as the "Amazon of South Korea".

Two Positive Attributes:

1. Active Customers Skyrocket, Fueling Growth Opportunities

As an online retailer, Coupang generates revenue growth by expanding its number of users and the average order size in dollars.

Over the last two years, Coupang’s active customers, a key performance metric for the company, increased by 11.9% annually to 23.6 million in the latest quarter. This growth rate is strong for a consumer internet business and indicates people love using its offerings.

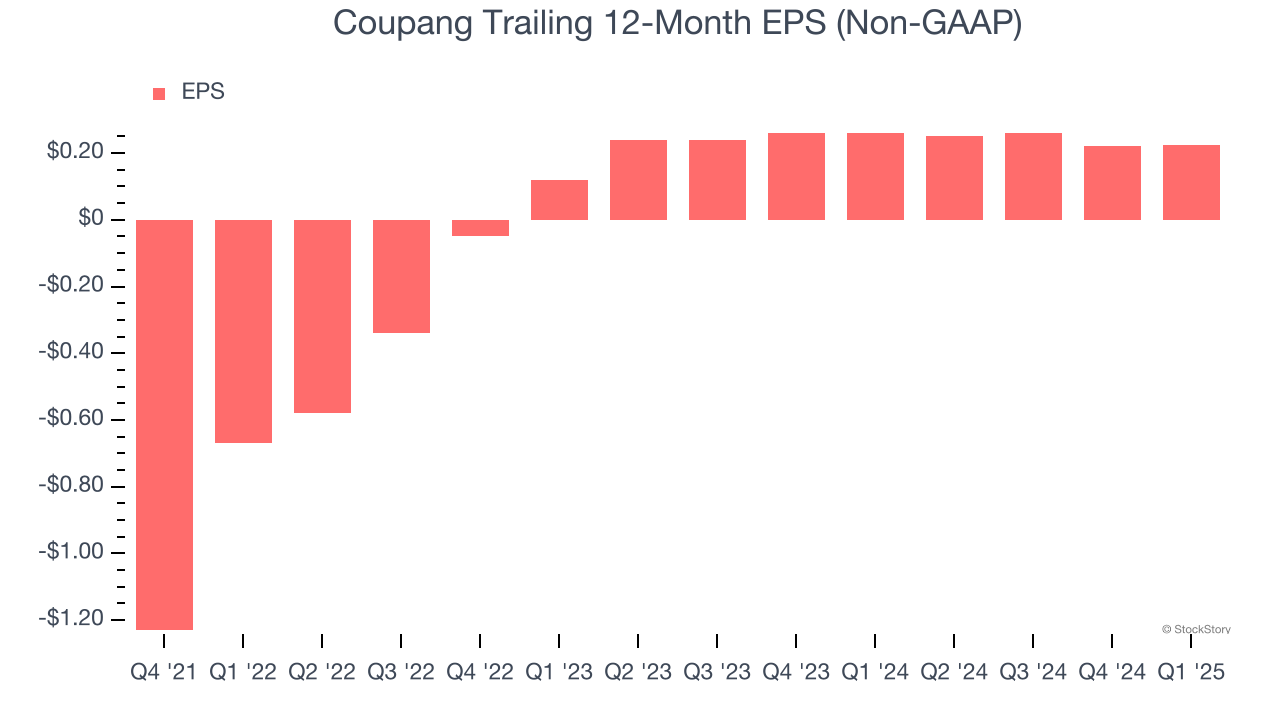

2. Outstanding Long-Term EPS Growth

Analyzing the change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Coupang’s full-year EPS flipped from negative to positive over the last three years. This is a good sign and shows it’s at an inflection point.

One Reason to be Careful:

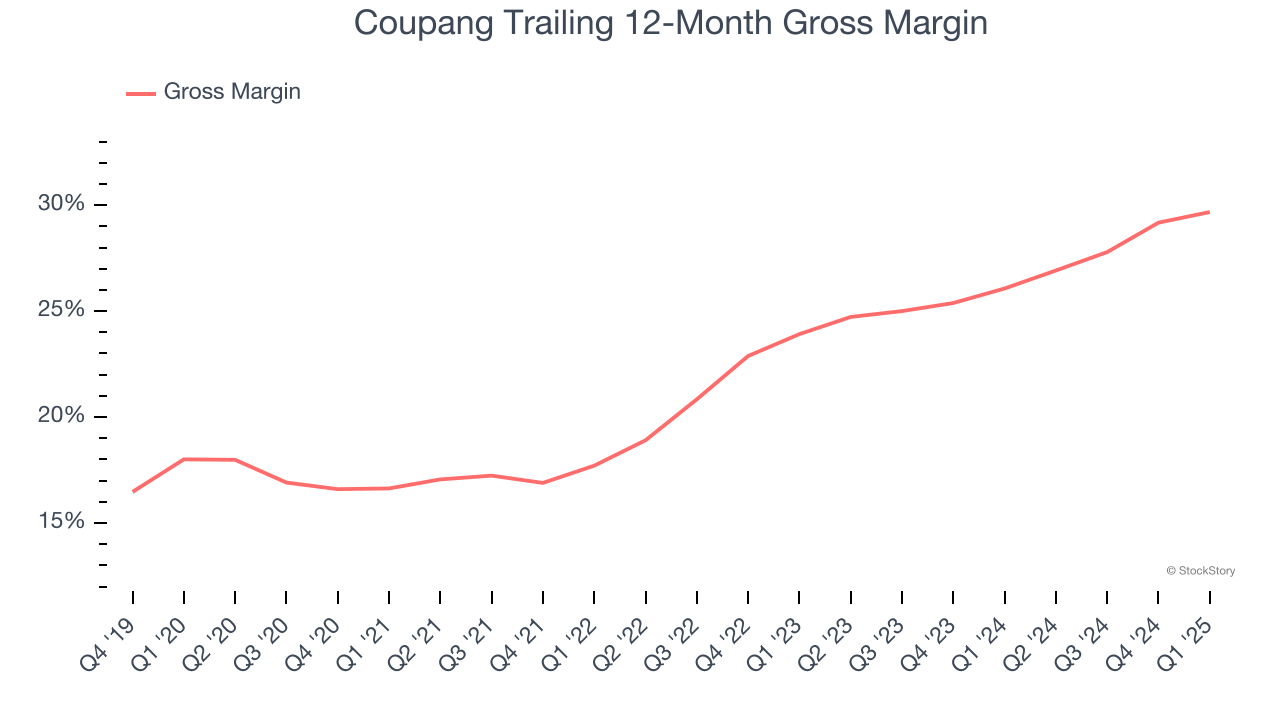

Low Gross Margin Reveals Weak Structural Profitability

For online retail (separate from online marketplaces) businesses like Coupang, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include the cost of acquiring the products sold, shipping and fulfillment, customer service, and digital infrastructure.

Coupang’s unit economics are far below other consumer internet companies because it must carry inventories as an online retailer. This means it has relatively higher capital intensity than a pure software business like Meta or Airbnb and signals it operates in a competitive market. As you can see below, it averaged a 28% gross margin over the last two years. Said differently, Coupang had to pay a chunky $71.96 to its service providers for every $100 in revenue.

Final Judgment

Coupang’s merits more than compensate for its flaws, and after the recent rally, the stock trades at 32.2× forward EV/EBITDA (or $31.23 per share). Is now a good time to buy despite the apparent froth? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Coupang

Donald Trump’s April 2024 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.